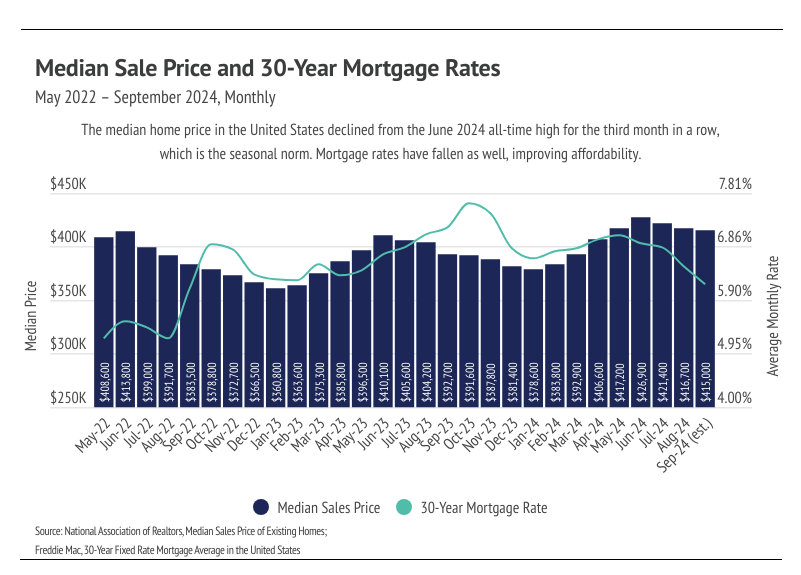

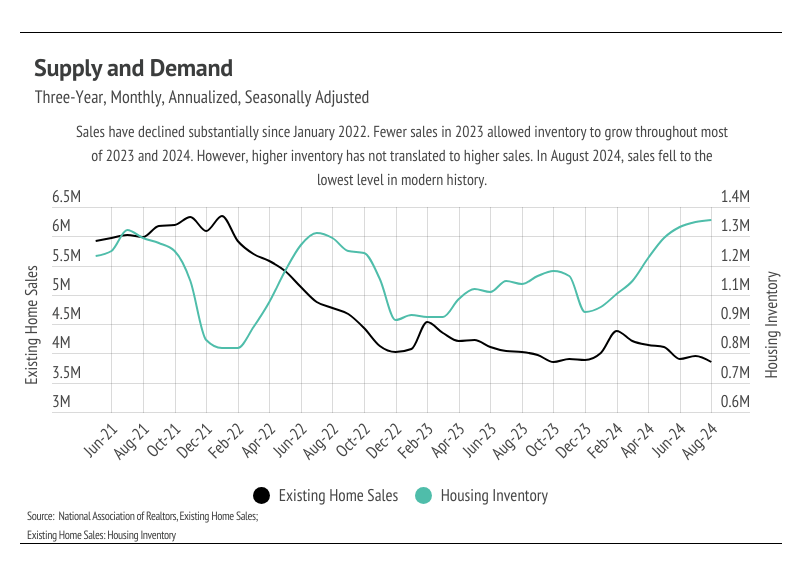

Enough data has been released to suggest that home prices peaked nationally in June 2024, and won’t peak again this year. Of course, there will be deviations in local markets, but the larger trend is clear: home prices are returning to a more normal growth and contraction cycle in which prices increase from January to June and contract from June to January. Sales have trended lower for nearly three years now, and that sales slowdown has allowed inventory to build to the highest level since 2020.

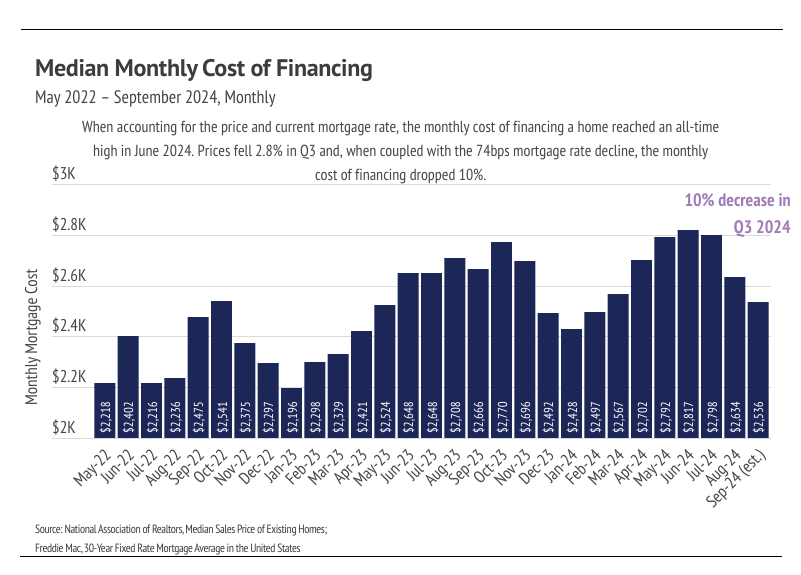

We were hopeful that sales would continue to increase this month due to the declining rates as it did last month, but sales fell to the lowest level in modern history. Even though the Fed lowered their benchmark rate by 0.50% at the September Fed meeting, mortgage rates weren’t largely affected, mainly because the rate cut was already priced into the current mortgage rates. In Q3 2024, the median price fell 2.8% and the mortgage rate declined by 74 bps, causing the payment on a monthly 30-year mortgage to drop 10%. Affordability is improving and the median home buyer saved $100,000 over the life of the loan, if they bought in September rather than June (a huge change in just three months!). Rate cuts and improved affordability are a promising sign as we look ahead to the spring market. We expect to enter 2025 with falling rates, high inventory, and seasonally lower home prices, which should create the perfect storm necessary for a hot spring market.

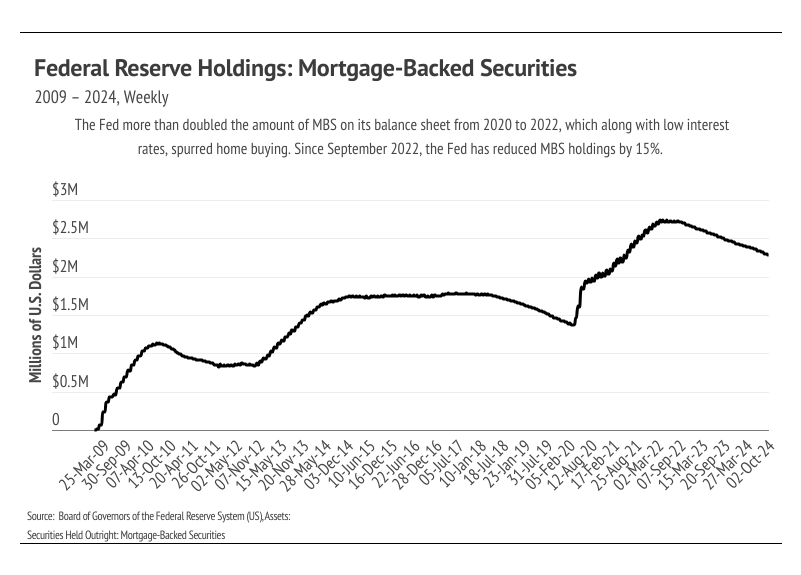

During the early pandemic, the Fed provided huge incentives to buy homes as part of its easy monetary policy by purchasing Mortgage-Backed Securities (MBS) and dropping interest rates. MBS play an integral role in home financing by allowing banks to bundle and sell mortgage loans, turning the bank into an intermediary between the financier and financial markets (investors). Banks get some fees, while investors (rather than the bank) get the interest and incur the risk from the bundle of mortgages. So, in many ways, the bank facilitates the loan but investors are the ones really lending the buyer the money. The Fed was a huge investor in 2020 and 2021, doubling its MBS holdings to $2.7 trillion by 2022. However, the Fed isn’t buying any more MBS and, in fact, has sold 15% ($4.16B) of its MBS holdings over the past two years. Even though rates are coming down, the MBS market has shifted to make loans less easy to originate, which has contributed to the market slowdown.

Last September, the average 30-year mortgage rate was 7.31%, meaning that a $500,000 loan would cost $3,431 per month. For reference, that same loan now costs $3,056 per month at 6.08%. Because the interest rate has such an outsized impact on the affordability of a home, fewer buyers entered the market, allowing inventory to build. Even though far fewer sales occurred over the past year, prices still rose, which they almost always do. This is actually a newer phenomenon, but one that isn’t going away. Since the mid-1990s, home prices began to move more like risk assets (stocks, bonds, commodities, etc.), which marked a huge change from the preceding 100 years. From 1890 to 1990, inflation-adjusted home prices rose only 12%, which is hard to imagine with the massive price growth, up 94% nationally, that we’ve seen over the past 10 years. All that to say, home prices over time really only move in one direction, which is up.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

BIG STORY DATA

THE LOCAL LOWDOWN

-

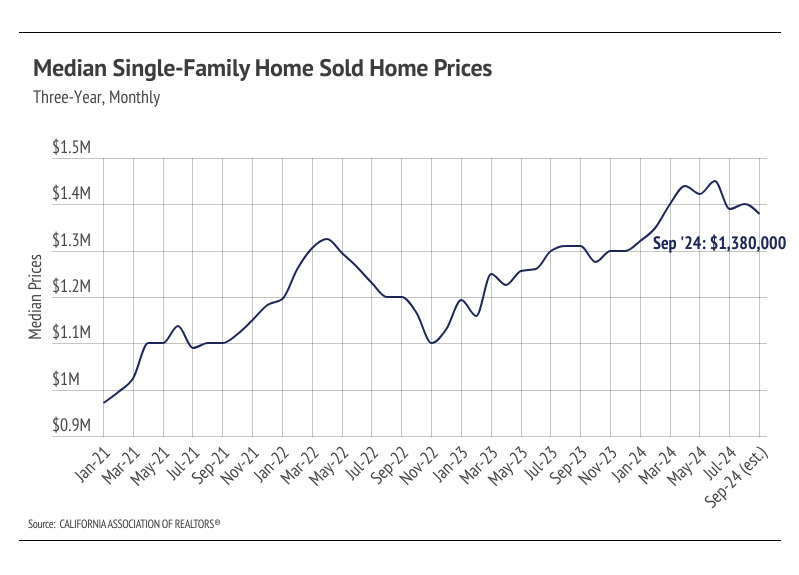

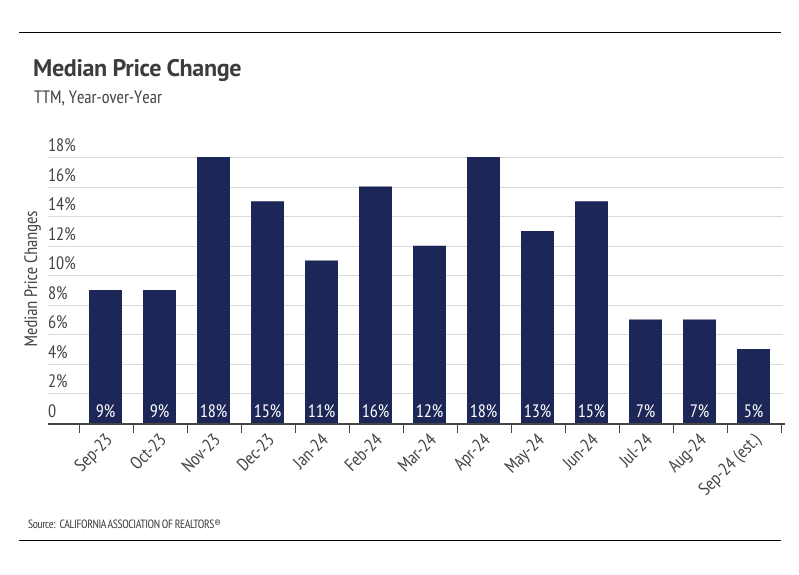

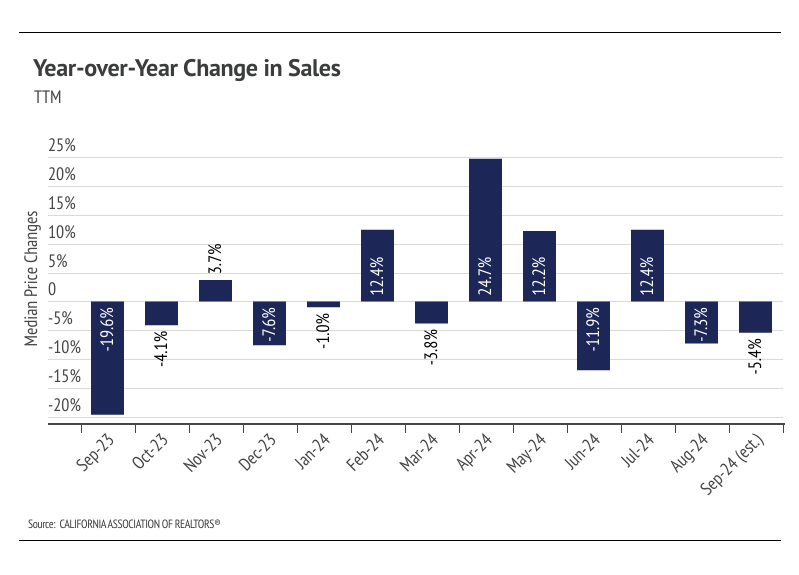

The median single-family home price rose in August, likely due to falling mortgage rates, but declined slightly in September. We expect price contractions in Q4, which is the seasonal norm.

-

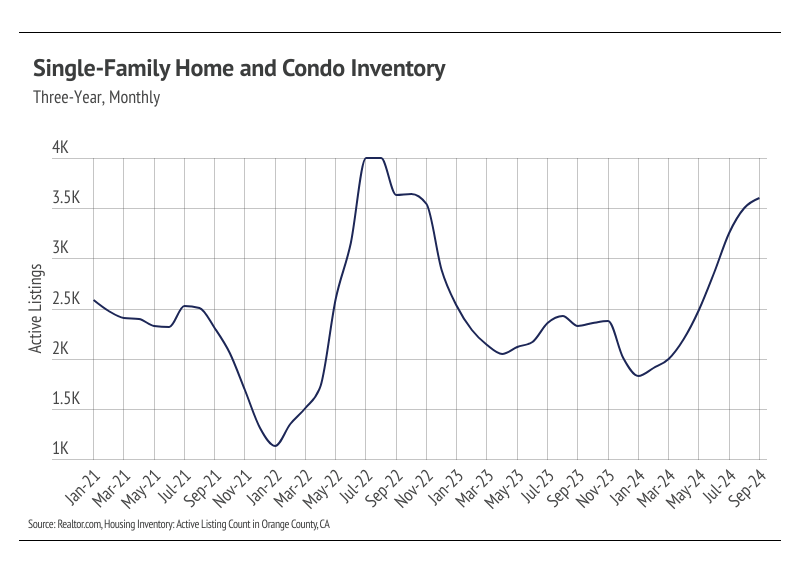

Inventory has doubled since the beginning of 2024. More homes on the market only benefits Orange County, which has been extremely undersupplied for the past four years.

-

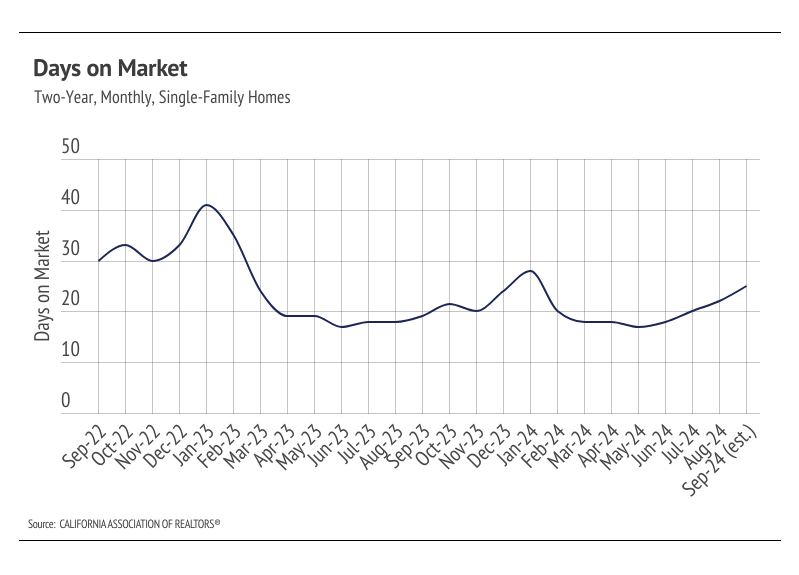

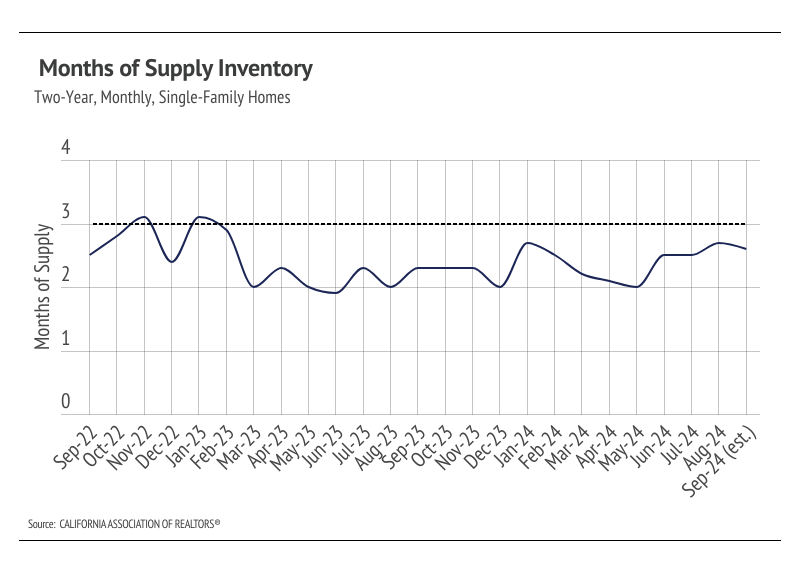

Months of Supply Inventory remained below three months of supply in September, indicating the market still favors sellers. Homes are still selling quickly, but Days on Market is moving slightly higher.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.